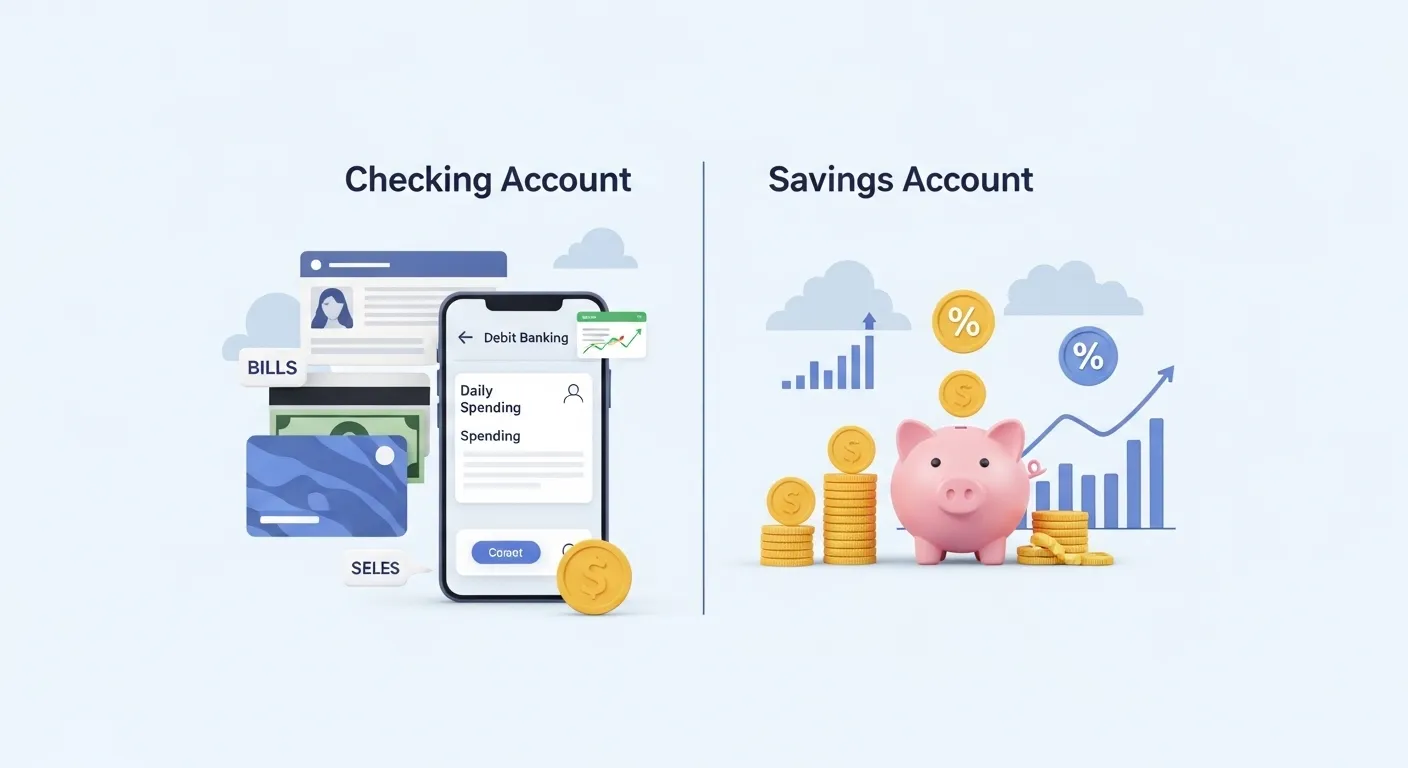

A young professional receives their first salary and wonders where to keep their money. They need easy access for daily expenses like groceries and bills, but they also want to save for future goals. This is where understanding the difference between checkings and savings becomes important. A checking account (often called “checkings” informally) is designed for frequent transactions, while a savings account helps store money securely and earn interest over time.

Many people confuse these two accounts, but knowing the difference between checkings and savings can improve financial decisions. Whether you are a student or a professional, understanding the difference between checkings and savings helps you manage money wisely. In fact, the difference between checkings and savings plays a key role in budgeting, saving, and achieving financial stability.

Key Difference Between Checkings and Savings

A checking account is used for daily transactions and easy access to money, while a savings account is used to store money and earn interest over time.

Why Is Their Difference Important for Learners and Experts?

For learners, understanding these accounts builds strong financial literacy. For experts, it ensures effective money management and financial planning. In society, checking accounts keep the economy active through daily transactions, while savings accounts promote financial security and future planning. Knowing their difference helps individuals avoid overspending and encourages disciplined saving habits.

Pronunciation

- Checkings (Checking Account)

- US: /ˈtʃekɪŋz/

- UK: /ˈtʃekɪŋz/

- Savings (Savings Account)

- US: /ˈseɪvɪŋz/

- UK: /ˈseɪvɪŋz/

Now, let’s dive deeper into the detailed difference between checkings and savings.

Difference Between Checkings and Savings

1. Purpose

- Checkings: Used for daily spending.

Example 1: Paying utility bills.

Example 2: Buying groceries with a debit card. - Savings: Used for storing money.

Example 1: Saving for a vacation.

Example 2: Building an emergency fund.

2. Accessibility

- Checkings: Easy and frequent access.

Example 1: ATM withdrawals anytime.

Example 2: Online payments. - Savings: Limited access.

Example 1: Withdrawal limits per month.

Example 2: Transfers with restrictions.

3. Interest

- Checkings: Usually little or no interest.

Example 1: Basic checking accounts.

Example 2: Salary accounts. - Savings: Earns interest.

Example 1: Bank savings account interest.

Example 2: High-yield savings accounts.

4. Transactions

- Checkings: Unlimited transactions.

Example 1: Daily purchases.

Example 2: Frequent transfers. - Savings: Limited transactions.

Example 1: Monthly withdrawal limits.

Example 2: Fewer transfers allowed.

5. Fees

- Checkings: May have more fees.

Example 1: Maintenance fees.

Example 2: ATM charges. - Savings: Usually fewer fees.

Example 1: Minimal maintenance fees.

Example 2: No fee for holding money.

6. Minimum Balance

- Checkings: Often low or none.

Example 1: Basic accounts.

Example 2: Student accounts. - Savings: Often requires a balance.

Example 1: Minimum deposit requirement.

Example 2: Penalty for low balance.

7. Risk of Spending

- Checkings: High risk of overspending.

Example 1: Easy card swipes.

Example 2: Frequent withdrawals. - Savings: Low risk of overspending.

Example 1: Withdrawal limits.

Example 2: Less frequent use.

8. Tools and Features

- Checkings: Includes debit cards and checks.

Example 1: Writing checks.

Example 2: Using a debit card. - Savings: Limited tools.

Example 1: Passbook accounts.

Example 2: Online tracking only.

9. Goal

- Checkings: Short-term use.

Example 1: Monthly expenses.

Example 2: Daily transactions. - Savings: Long-term goals.

Example 1: Buying a house.

Example 2: Education fund.

10. Growth

- Checkings: No growth focus.

Example 1: Money stays the same.

Example 2: Used quickly. - Savings: Encourages growth.

Example 1: Interest adds value.

Example 2: Long-term accumulation.

Nature and Behaviour

- Checkings: Active, flexible, and transaction-focused. It is used regularly and supports daily financial activities.

- Savings: Passive, secure, and growth-oriented. It is designed to protect and increase money over time.

Why Are People Confused?

People often confuse these accounts because both are offered by banks and involve storing money. The similar names and overlapping features, such as online access, also create confusion, especially for beginners.

Table: Difference and Similarity

| Aspect | Checkings | Savings | Similarity |

| Purpose | Daily use | Saving money | Both store money |

| Access | High | Limited | Both accessible via banks |

| Interest | Low/None | Higher | Both may earn interest |

| Transactions | Frequent | Limited | Both allow transfers |

| Safety | Secure | Secure | Both are bank-protected |

Which Is Better in What Situation?

A checking account is better for everyday financial activities. It allows easy access to money, making it ideal for paying bills, shopping, and handling daily expenses. If you need flexibility and quick transactions, a checking account is the best choice.

A savings account is better for future planning. It helps you store money safely while earning interest over time. If your goal is to build wealth, save for emergencies, or achieve long-term financial goals, a savings account is the better option.

Metaphors and Similes

- Checkings: “A checking account is like a wallet you use every day.”

- Savings: “A savings account is like a treasure chest for the future.”

Connotative Meanings

- Checkings

- Positive: Convenience, accessibility

Example: Easy access to money - Negative: Overspending

Example: Spending without thinking

- Positive: Convenience, accessibility

- Savings

- Positive: Security, discipline

Example: Building financial stability - Neutral: Reserved funds

Example: Money set aside

- Positive: Security, discipline

Idioms and Proverbs

- “Save for a rainy day”

Example: Always save for a rainy day using a savings account. - “Live paycheck to paycheck”

Example: Without savings, people may live paycheck to paycheck using only checking accounts.

Works in Literature

- The Richest Man in Babylon — Finance, George S. Clason, 1926

- Your Money or Your Life — Personal Finance, Vicki Robin & Joe Dominguez, 1992

Movies Related to Finance

- The Pursuit of Happyness — 2006, USA

- The Big Short — 2015, USA

FAQs

1. Can I have both accounts?

Yes, most people use both for better money management.

2. Which account earns more interest?

Savings accounts usually earn more interest.

3. Is checking safer than savings?

Both are equally secure in banks.

4. Can I transfer money between them?

Yes, transfers are usually easy and quick.

5. Which is better for daily use?

Checking accounts are better for daily transactions.

How Both Are Useful for Surroundings

Checking accounts keep daily financial activities smooth and efficient, while savings accounts promote stability and future planning. Together, they support individuals, families, and the economy by balancing spending and saving habits.

Final Words for Both

Checking accounts manage your present, while savings accounts protect your future. Both are essential tools for a balanced financial life.

Conclusion

Understanding the difference between checkings and savings is essential for effective financial management. Checking accounts provide easy access for daily expenses, while savings accounts help build financial security over time. Both serve unique purposes and complement each other in managing money wisely. By using them correctly, individuals can achieve financial stability and long-term success. Whether you are starting your financial journey or improving your skills, knowing their difference ensures smarter decisions and a better future.

I am a professional SEO content writer specialising in comparison-based and grammar-focused articles. Through my website GrammarCompare.com, I help readers clearly understand the difference between confusing terms with well-researched, easy-to-read content. My expertise lies in focusing on clarity, accuracy, and practical explanations that improve both knowledge and writing skills.